Canada Pushes Forward with Sustainability Disclosure Standards

The Canadian Sustainability Standards Board (CSSB) is moving to establish sustainability disclosure standards for Canadian companies. On March 13, 2024, CSSB published two exposure drafts for the Canadian Sustainability Disclosure Standards (CSDS) – CSDS 1 and CSDS 2 – and announced the opening of a public consultation period during which it will collect feedback on the proposed Standards for the Canadian. Following the end of the 90-day consultation period on June 10, 2024, CSSB will aim to finalize the standards by the end of the fourth quarter of 2024, marking another milestone towards the adoption of sustainability disclosure standards in Canada.

The Canadian Securities Administrators (CSA) is then expected to integrate the final CSSB standards into its own proposed rules on mandatory climate-related disclosures. However, the CSA anticipates adopting only the provisions of the CSSB standards relevant to supporting climate-related disclosures.

Disclosure Requirements and Timelines

The disclosure requirements of the draft CSSB standards closely follow the International Sustainability Standards Board’s (ISSB) IFRS S1 and S2 and will facilitate the alignment of Canadian entities with international reporting standards. Like the ISSB’s structure, CSDS 1 requires companies to disclose sustainability-related risks and opportunities, and CSDS 2 requires companies to disclose climate-related risks and opportunities. Additionally, both standards adopt the four pillars established by the Taskforce for Climate-related Financial Disclosures (TCFD) framework: Governance, Strategy, Risk Management, and Metrics & Targets.

Compared with the ISSB standards, three notable distinctions in the CSSB standards include:

- Effective Date. Whereas the ISSB standards apply to entities for the reporting periods starting on or after Jan. 1, 2024, the CSSB standards will begin to apply for reporting periods starting on or after Jan. 1, 2025. This delay takes into consideration the timing of issuance for the CSSB standards.

- Extended transition relief. The standards allow for later reporting of disclosures related to sustainability-related risks and opportunities. This relief extends to both the inclusion of sustainability-related risks and opportunities (as outlined in CSDS 1) and the disclosure of comparative information.

- Scope 3 disclosure timelines. Extended relief for the disclosure of Scope 3 emissions by one additional year.

Market Preparedness

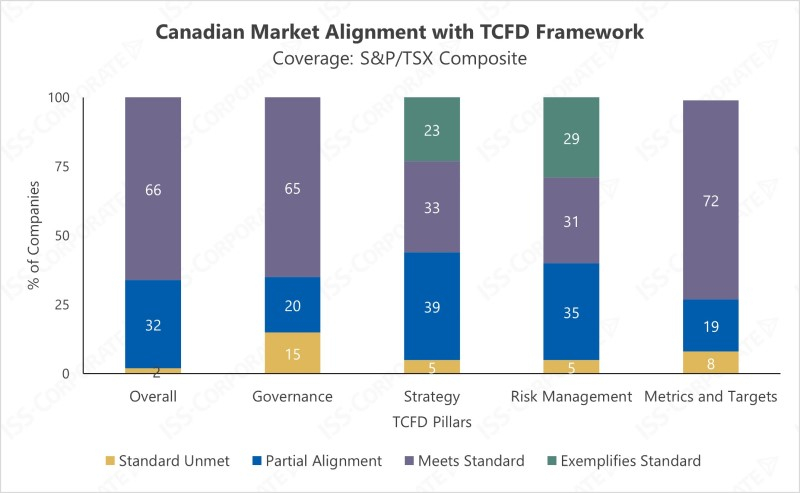

To assess the level of preparedness in aligning with the draft CSSB standards among Canadian companies, ISS-Corporate assessed companies’ current alignment with the TCFD framework, based on recent disclosures. Disclosure alignment with the TCFD framework can serve as a relevant proxy, as TCFD effectively serves as the foundation of IFRS S2 and CSDS 2.

Source: ISS-Corporate Climate Analytics, as of May 31, 2024

Approximately two-thirds of Canadian companies under review (representing the largest companies in the market as constituents of the TSX Composite Index) were found to be aligned with the TCFD framework overall, while the other third showed at least partial alignment or an indication of initial measures taken toward reporting under the framework.

While a considerable number of companies have taken steps to align with the TCFD framework, few Canadian companies demonstrated exemplary practices consistent with global leaders in deeply integrating the framework into all aspects of reporting. Some companies were exemplary in the areas of climate strategy and risk management, even though those are the two pillars where the overall level of alignment is generally lower than the pillars of Governance and Metrics and Targets.

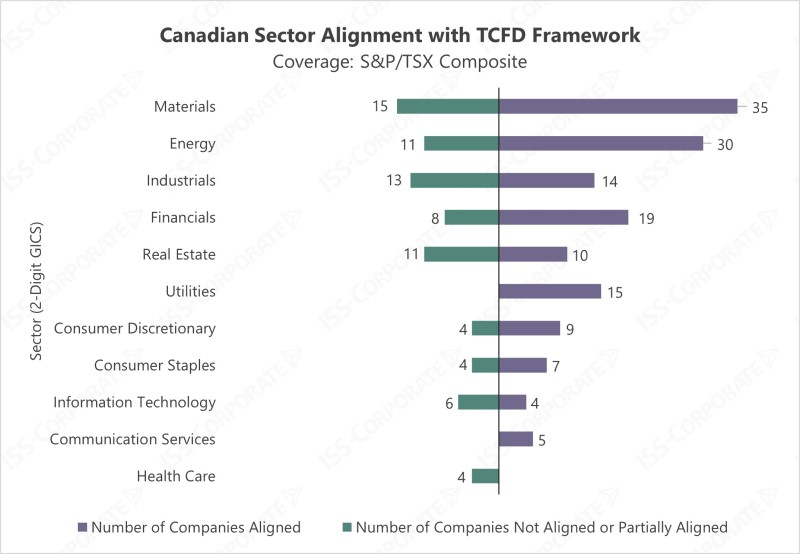

Source: ISS-Corporate Climate Analytics, as of May 31, 2024

The Materials, Energy, and Financials sectors, all exhibit strong levels of preparedness in current and anticipated climate disclosures under the draft CSSB standards. More than 70% of companies under review in these three sectors, representing a significant portion of Canada’s economy, demonstrate alignment with the TCFD reporting framework. Companies in the Utilities and Communications Services sectors show alignment with the standard, indicating these sectors are well-positioned to transition into future climate disclosure requirements. Conversely, the Real Estate, Information Technology, and Health Care sectors all exhibit lower levels of preparedness, with less than 50% of companies in alignment with the TCFD recommendations.

Key Considerations

Efforts to develop a sustainability disclosure standard aligned with ISSB in Canada are consistent with the global trend toward the adoption of a universal framework for mandatory sustainability reporting.

Companies that have already aligned their climate disclosures with the TCFD framework are well-prepared to begin the transition to the CSSB standards. However, the transition reliefs provided indicate that some Canadian businesses need to re-assess their approach to the expansion of sustainability disclosures beyond climate-related risks and opportunities, presenting a new challenge for organizations to develop more robust risk assessment and data collection processes.

Related Publications

- Mapping TCFD to the IFRS S2 on Climate Disclosures

While based on TCFD, IFRS S2 significantly expands the scope and detail of disclosures required. To assess the concrete implications of this progression, ISS-Corporate performed a detailed cross-standard analysis, asking two key questions: What are the additional disclosures required under IFRS S2? And how well do exemplary climate reports align with IFRS S2? - Mandatory Climate Disclosure in South Korea

The Korea Sustainability Standards Board (KSSB) published the Exposure Draft of the ‘Korean Sustainability Disclosure Standards’ on May 2. While the exact scope and timing of the initiative are yet to be unveiled, starting from 2026, climate-related disclosures will become mandatory. - Sustainability Disclosures in Asia-Pacific: Accelerated Transition to New Standards

ISS-Corporate reviewed the level of alignment of corporate disclosures in major Asia-Pacific markets with established frameworks – the Global Reporting Initiative (GRI), the Sustainability Accounting Standards Board standards, and the Taskforce on Climate-related Financial Disclosures (TCFD) recommendations – to identify which countries and sectors are better prepared to meet the more ambitious requirements of CSRD and the IFRS Sustainability Disclosure Standards.