Materiality Assessments: Expectations and Best Practices

Materiality Assessments Evolve as Key Tool for Corporate Sustainability Management

Over the past decade, the business world has made significant strides in establishing standardized and methodical approaches for corporates developing their sustainability strategies and relevant disclosures. Today, a materiality assessment for identifying and prioritizing key issues has become a basic expectation among stakeholders, with certain jurisdictions beginning to require companies to conduct such assessments according to prescribed standards, including assurance requirements.

Through stakeholder engagement and data analysis, materiality assessments can be instrumental tools for companies to identify, manage, and communicate their impacts, risks, and opportunities. Several standards and regulations have established guidance or set expectations for companies to conduct materiality assessments, including the IFRS S1 and S2 (and the legacy TCFD and SASB standards) and GRI. Globally, regulations also set these expectations, with the EU’s European Sustainability Reporting Standards (ESRS) emerging as the preeminent standard for double materiality assessments.

Evaluating Materiality Assessment Disclosures Globally

ISS-Corporate reviewed corporate disclosure data on whether companies conduct an evaluation of material sustainability topics. As demonstrated in the graph below, companies in the Americas lag their counterparts in Asia Pacific and EMEA in terms of disclosing an evaluation of the materiality of sustainability-related topics across all market cap categories.

Alignment with Reporting Frameworks

As mentioned above, GRI is one of the standards that has set an expectation for companies to determine their material topics. While GRI supports the concept of double materiality, the standards primarily focus on impact materiality. Companies that align their sustainability-related disclosures with the GRI standards are well-suited to also address financial materiality due to a sequencing effect. Once companies identify their actual and potential positive and negative impacts (impact materiality), they can determine if and how these impacts pose a risk or opportunity for the company’s financial health and value creation (financial materiality).

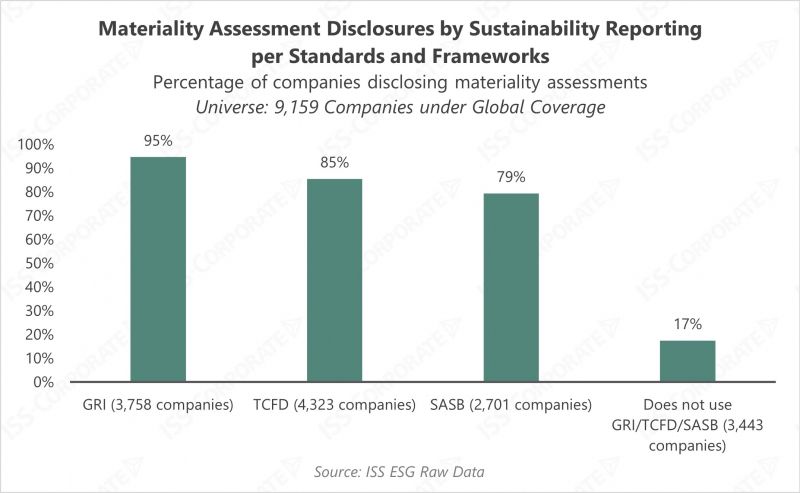

ISS-Corporate reviewed the corporate disclosure data to determine the relationship between companies who disclose their sustainability reporting is informed by the GRI Standards and companies who disclose an evaluation of the material sustainability topics. As demonstrated in the graph below, 95% of companies whose disclosures are informed by GRI have evaluated the materiality of sustainability topics. This finding suggests that GRI can serve as a helpful standard to consider as a starting point in preparation for compliance with regulatory mandates requiring the completion of a materiality assessment.

Additionally, companies whose disclosures are informed by the TCFD and SASB frameworks (currently both under the auspices of the International Sustainability Standards Board) are also more likely to perform materiality assessments. To help companies prioritize their sustainability disclosures the SASB standards identify material sustainability topics for each industry, with an emphasis on financial materiality. The prevalence of materiality assessments among companies whose disclosures are informed by established standards and frameworks indicates a more systematic approach and a higher level of maturity in sustainability reporting among these firms. On the contrary, among companies that did not leverage any of these frameworks for their disclosures, only 17% provided disclosures confirming that they had assessed the materiality of key sustainability issues.

Materiality Assessments and Engagements in Shareholder Proposals

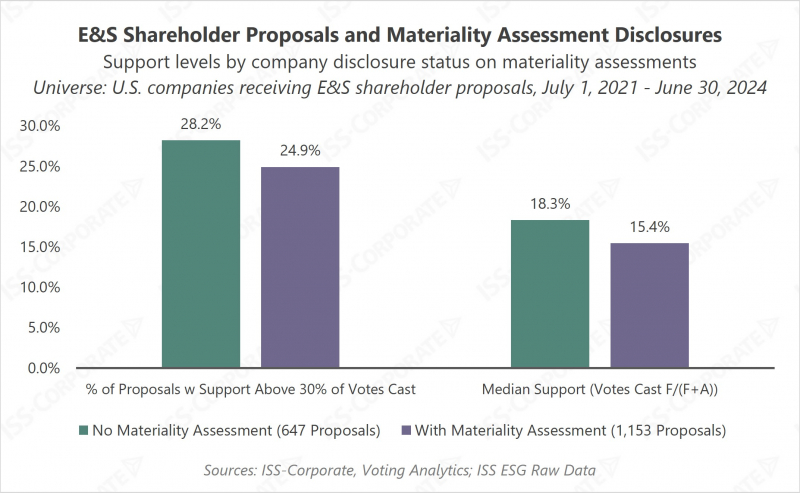

Understanding stakeholders’ perspectives is best practice for materiality assessments. Companies who account for their stakeholders’ perspectives are more likely to have positive outcomes from their stakeholder engagements. As an example, ISS-Corporate reviewed data regarding environmental and social shareholder proposals in the past three years and the outcomes of these requests depending on whether the target company had conducted a materiality assessment or not. The graph below shows that shareholder proposals submitted at companies with materiality assessment disclosures received lower levels of support. This trend suggests that these companies likely engaged with their shareholders in a more effective manner, as proposals with lower support levels generally indicate that shareholders believe the company is adequately addressing the topic at hand.

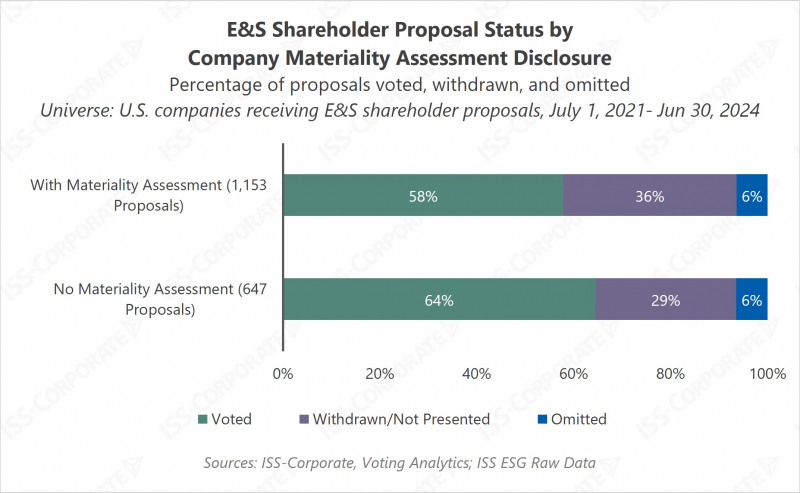

In addition, companies that received shareholder proposals and had conducted a materiality assessment were more likely to see proposals withdrawn from proponents compared to companies that had not conducted a materiality assessment. The graph below shows these more positive outcomes for companies that conducted materiality assessments, as withdrawals amounted to 36% of submitted proposals for these companies, compared to 29% percent for companies that had not conducted materiality assessments. A proposal withdrawal typically suggests that the target company engaged with the proponent to address the underlying issues to the proponent’s satisfaction.

Best Practices for Corporates Starting a Materiality Assessment

Given growing expectations around the disclosure and management of materiality assessments and the interconnectedness of regulatory requirements and disclosure standards, companies worldwide will be expected to focus on developing these processes as a foundation for their sustainability programs. For companies starting materiality assessments, here are some best practices to consider (informed by key concepts shared by the ESRS standards and relevant implementation guidance):

- Apply the double materiality principle, including both impact and financial materiality.

- Assess materiality across the value chain, starting with mapping potential impacts, risks and opportunities both upstream and downstream in relation to the organization’s business partnerships, operations, and products and services.

- Understand stakeholders’ perspectives, including both affected stakeholders and the key audience of the sustainability statements. This exercise involves both stakeholder mapping and a robust stakeholder engagement program.

- Consider both actual and potential impacts, including the scope of the impact, the level of severity.

- Factor in resource dependencies, including human, natural, and social resources, which may play an important role on determining impact and financial materiality.

- Leverage robust processes for conducting materiality assessments that allow for assurance-readiness as well as a regular and systematic review and evaluation of material issues.